Comfort Systems USA’s Q1 2026: A Blowout Quarter Powered by Tech, Manufacturing, and a Massive Backlog

Comfort Systems USA, Inc. had the kind of quarter that gets attention.

In its Form 10-Q filed on April 17, 2026, the company reported results for the three months ended March 31, 2026—and the numbers were striking. Revenue jumped more than 50%, net income more than doubled, cash flow swung sharply positive, and backlog climbed to a record level.

For a company operating in mechanical and electrical contracting, that kind of performance says a lot about both execution and demand. Comfort Systems is not just benefiting from a favorable market; it appears to be converting that demand into higher margins, stronger cash generation, and a bigger future revenue pipeline.

Let’s break down what happened, what drove the quarter, and what risks still matter.

The Headline: Revenue Surged 56.5%

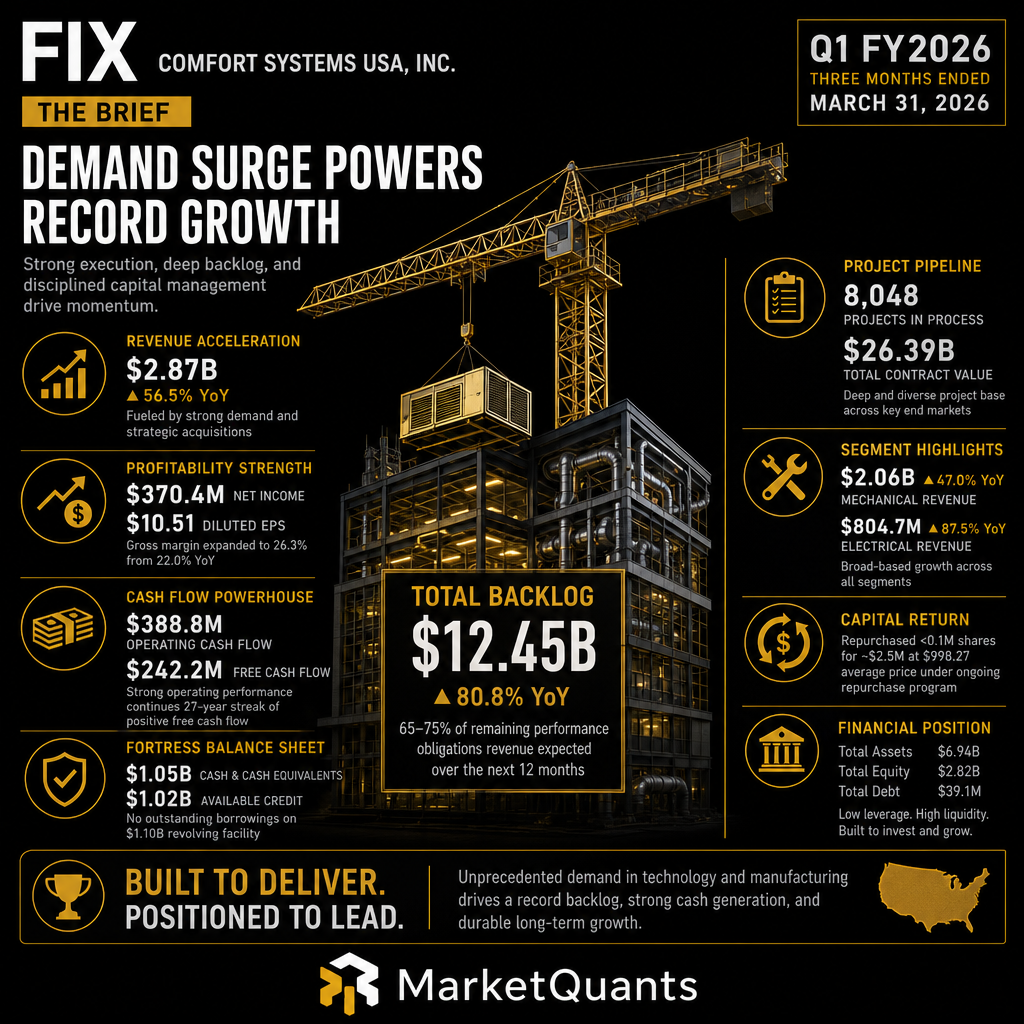

Comfort Systems USA reported consolidated revenue of $2.87 billion for Q1 2026, compared with $1.83 billion in Q1 2025.

That’s a year-over-year increase of 56.5%.

For a construction and contracting services company, this is a very large jump—especially in the first quarter, which is often seasonally softer for the mechanical and electrical contracting industries.

The company’s growth was supported by strong demand across key end markets, especially:

- Technology

- Manufacturing

- Healthcare

- New construction projects

- Mechanical and electrical infrastructure work

According to the filing, same-store revenue growth was particularly strong, helped by demand from technology and manufacturing customers. Acquisitions completed in 2025 also contributed to the expanded revenue base.

Profitability Was Even More Impressive

Revenue growth is great, but revenue without profit is not very exciting. Comfort Systems’ Q1 2026 stood out because profit grew even faster than sales.

Net income for the quarter was $370.4 million, compared with $169.3 million in Q1 2025.

That means net income increased by approximately 119% year over year.

Basic income per share rose to $10.52, up from $4.77 in the prior-year period.

That’s a major improvement and reflects not only higher business volume but also stronger operating leverage and margin expansion.

Gross Margin Expanded Meaningfully

One of the most important metrics in the quarter was gross profit percentage.

Comfort Systems reported a gross profit percentage of 26.3% in Q1 2026, up from 22.0% in Q1 2025.

That improvement matters because construction and contracting companies often face pressure from labor costs, materials inflation, project timing, and competitive bidding. Expanding gross margin in that environment suggests strong project execution, favorable mix, and disciplined pricing.

In plain English: the company did not just take on more work—it appears to have taken on better or better-managed work.

SG&A Stayed Under Control

Selling, general, and administrative expenses were 9.4% of revenue in Q1 2026.

As companies grow quickly, overhead can sometimes balloon alongside revenue. But Comfort Systems’ SG&A ratio suggests it maintained operating discipline while scaling.

That’s one reason net income growth outpaced revenue growth. The company benefited from a larger revenue base while keeping administrative costs relatively efficient as a percentage of sales.

Backlog Hit $12.45 Billion

If there is one number that really captures the strength of Comfort Systems’ demand environment, it is backlog.

As of March 31, 2026, total backlog reached $12.45 billion.

That represents:

- An 80.8% increase from March 31, 2025

- A 4.3% increase from December 31, 2025

Backlog is not the same as guaranteed revenue, but it is an important indicator of future work. For Comfort Systems, a backlog of this size suggests that demand remains deep and broad, particularly in large-scale projects tied to technology and manufacturing infrastructure.

It also provides a degree of visibility into future revenue. That visibility is especially valuable in a cyclical industry like construction.

Technology Customers Are Driving the Story

One of the most interesting takeaways from the quarter is the company’s customer mix.

For Q1 2026, revenue by customer type was led by:

| Customer Type | Share of Q1 2026 Revenue |

|---|---|

| Technology | 56.4% |

| Manufacturing | 18.7% |

| Healthcare | 7.7% |

Technology was by far the largest category, representing more than half of total revenue.

That is a huge detail.

Comfort Systems is not simply a traditional HVAC or mechanical contractor serving ordinary commercial buildings. Increasingly, it is tied to major infrastructure needs in high-growth sectors. Technology-related projects can include complex facilities that require sophisticated mechanical and electrical systems—think data centers, advanced manufacturing sites, clean rooms, and other mission-critical infrastructure.

Manufacturing was also a major contributor, accounting for nearly one-fifth of revenue. This aligns with broader trends in reshoring, industrial expansion, semiconductor investment, and advanced production facilities across the United States.

New Construction Dominated Revenue

By activity type, new construction accounted for 74.5% of revenue in Q1 2026.

That tells us Comfort Systems is heavily exposed to new project development rather than only maintenance, retrofit, or service work.

This can be a positive when demand is strong, as it clearly is right now. Large new construction projects can create meaningful revenue opportunities and build backlog quickly.

However, it also means the company remains exposed to construction cycles. If economic conditions weaken or project starts slow, new construction activity can be affected.

For now, though, Comfort Systems appears to be operating in a very favorable demand environment.

Mechanical Segment: The Core Revenue Engine

Comfort Systems operates through two primary segments: Mechanical and Electrical.

The Mechanical Segment remained the larger of the two in Q1 2026, generating $2.06 billion in revenue.

That represented 71.9% of total company revenue.

Mechanical Segment revenue increased 47.0% year over year, a strong growth rate for a segment already operating at significant scale.

Mechanical services can include heating, ventilation, air conditioning, plumbing, piping, controls, and related systems. These services are essential in complex commercial and industrial buildings, particularly in technology and manufacturing facilities where environmental control, reliability, and efficiency are critical.

Electrical Segment: Smaller, But Growing Faster

The Electrical Segment generated $804.7 million in Q1 2026 revenue, representing 28.1% of total revenue.

Even more notable: Electrical Segment revenue increased 87.5% year over year.

That is exceptional growth.

Electrical capabilities are increasingly important for Comfort Systems’ customer base. Technology and advanced manufacturing facilities require substantial electrical infrastructure, from power distribution to controls, automation, backup systems, and specialized installations.

The rapid expansion of the Electrical Segment may also reflect the impact of recent acquisitions and increased demand for integrated mechanical and electrical contracting solutions.

Acquisitions Helped Expand the Platform

Comfort Systems completed multiple acquisitions in 2025, including:

- Feyen Zylstra

- Meisner Electric

- Right Way Plumbing & Mechanical

These acquisitions contributed to revenue, backlog, and broader market presence.

Strategic acquisitions can be especially valuable in the mechanical and electrical contracting industry because local expertise, customer relationships, skilled labor, and regional reputation all matter. By acquiring established operators, Comfort Systems can expand its geographic reach, deepen capabilities, and participate in more large-scale projects.

The key question with acquisitions is always integration. Based on the Q1 2026 numbers, the company appears to be absorbing its expanded operations while continuing to deliver strong financial results.

Cash Flow Swung Sharply Positive

Another standout metric was operating cash flow.

Comfort Systems generated $388.8 million in net cash provided by operating activities in Q1 2026.

In Q1 2025, the company used $88.0 million in operating cash.

That is a dramatic swing.

Strong operating cash flow gives the company flexibility. It can support organic growth, fund acquisitions, invest in working capital, maintain liquidity, and return capital to shareholders.

For a project-based business, cash flow can fluctuate depending on billing schedules, project timing, collections, and working capital needs. Still, the Q1 2026 improvement was significant and reinforces the strength of the quarter.

The Balance Sheet Looks Very Strong

As of March 31, 2026, Comfort Systems reported:

- Total assets: $6.94 billion

- Total stockholders’ equity: $2.82 billion

- Cash and cash equivalents: $1.05 billion

The company also had no outstanding borrowings on its $1.10 billion revolving credit facility.

Available credit under that facility was approximately $1.02 billion.

That liquidity position is a major advantage. It gives Comfort Systems room to maneuver, particularly in an industry where bonding capacity, working capital, and financial strength can influence the ability to win and execute large projects.

Capital Allocation: Modest Share Repurchases

During Q1 2026, Comfort Systems repurchased 2,553 shares for approximately $2.5 million.

The average purchase price was $998.27 per share.

This was not a massive buyback relative to the company’s scale or cash position, but it does show that share repurchases remain part of the capital allocation toolkit.

Given the company’s growth and acquisition opportunities, management may be prioritizing financial flexibility over aggressive buybacks—and with backlog and demand running at elevated levels, that approach makes sense.

Why This Quarter Matters

Comfort Systems’ Q1 2026 results were important for several reasons.

First, the company demonstrated that demand remains exceptionally strong in its core markets.

Second, the company translated that demand into higher margins and significantly higher earnings.

Third, backlog continued to grow from already elevated levels.

Fourth, the balance sheet remained clean, with substantial cash and no revolver borrowings.

Together, those factors paint a picture of a company operating from a position of strength.

The Big Growth Drivers

The quarter’s performance appears to have been driven by a combination of structural and company-specific factors.

1. Technology Infrastructure Demand

Technology customers accounted for 56.4% of Q1 2026 revenue. That level of exposure suggests Comfort Systems is benefiting from major investments in digital infrastructure, data capacity, automation, and complex facility construction.

2. Manufacturing Expansion

Manufacturing contributed 18.7% of revenue. The U.S. manufacturing buildout remains a powerful theme, especially in advanced manufacturing, semiconductor-related projects, and industrial modernization.

3. Large New Construction Projects

With new construction accounting for 74.5% of revenue, Comfort Systems is benefiting from major project activity rather than relying solely on smaller service work.

4. Segment Expansion

Both Mechanical and Electrical grew substantially, with the Electrical Segment growing especially fast. This strengthens Comfort Systems’ ability to offer broader solutions across complex projects.

5. Acquisitions

Recent acquisitions expanded the company’s footprint and capabilities, contributing to revenue and backlog growth.

Risks to Watch

As strong as the quarter was, there are still risks worth watching.

Labor Cost Pressure

The company expects increased labor costs to remain a challenge. Skilled labor is critical in mechanical and electrical contracting, and labor availability can affect both margins and project timelines.

Supply Chain Delays

Comfort Systems also expects intermittent supply chain delays to persist over the next several quarters. Delays in equipment, materials, or specialized components can disrupt project execution and affect working capital.

Competitive Pricing

The company operates in markets where local and regional competitors remain active. Price competition is expected to continue, which can pressure margins if bidding becomes more aggressive.

Cyclicality

Construction is cyclical. If economic conditions weaken, project starts or customer capital spending could slow.

Seasonality

The mechanical and electrical contracting industries are subject to seasonal patterns, with the first quarter typically seeing lower demand. Comfort Systems overcame that seasonality in Q1 2026, but it remains a factor in year-to-year comparisons.

Bonding and Insurance Exposure

Surety bonds are historically required for roughly 10% to 20% of the company’s business. If sureties became less willing to issue performance and payment bonds, it could affect project opportunities.

The company is also self-insured for various liabilities, including workers’ compensation, auto, and general liability. These estimates are reviewed quarterly by a third-party actuary, but claims experience can still affect results.

Interest Rate Risk

Comfort Systems has exposure to market risk related to interest rates. However, with no outstanding borrowings on its revolving credit facility as of quarter-end, this risk appears manageable at the moment.

A Strong Quarter, But Expectations May Be High

One thing to keep in mind: when a company reports numbers this strong, expectations can rise quickly.

Revenue growth of 56.5%, net income growth of more than 100%, and backlog growth of 80.8% are not ordinary results. Investors and analysts may start expecting continued exceptional performance.

That can create pressure. Even if the business remains healthy, future comparisons could become more difficult.

The real question is not simply whether Comfort Systems had a great Q1. It clearly did.

The better question is whether the company can sustain elevated revenue, margins, and backlog conversion over the next several quarters.

Final Thoughts

Comfort Systems USA delivered an outstanding Q1 2026.

The company reported:

- $2.87 billion in revenue

- $370.4 million in net income

- $10.52 in basic income per share

- 26.3% gross profit margin

- $12.45 billion in backlog

- $388.8 million in operating cash flow

- $1.05 billion in cash and equivalents

- No outstanding borrowings on its revolving credit facility

That combination of growth, profitability, backlog, and liquidity is impressive.

The quarter also highlights Comfort Systems’ increasingly important role in building and supporting the infrastructure behind technology and manufacturing growth in the United States. With technology customers representing more than half of quarterly revenue, the company appears closely tied to some of the strongest construction demand themes in the market.

Of course, risks remain. Labor costs, supply chain delays, competitive pricing, and construction cyclicality are all worth monitoring. But as of Q1 2026, Comfort Systems looks financially strong, operationally effective, and well positioned in attractive end markets.

In short: this was not just a good quarter. It was a statement quarter.